To SMA clients and friends of Vailshire Capital Management:

- From my vantage point, the US economy is still resilient–thanks, in part, to massive fiscal spending

- I continue to believe that the 2020s will generally be an unkind decade for stocks and bonds… the bread and butter of typical 60/40 Wall Street portfolios

- Bonds were slated (by me) to perform quite poorly this decade, after a decade-long stint of near-zero or zero interest rate policies (ZIRP). As you may have noticed, Treasuries quickly obliged to this expectation

Current Market Conditions

Ongoing Liquidity Suck

Hello from Colorado Springs!

——–

The latest episode of Bitcoin Fundamentals on The Investor’s Podcast with the Bitcoin and Mastermind group will be released later today, after I finish this update. The panel includes Preston Pysh (the host), Joe Carlasare, Steven McClurg, and myself (@VailshireCap).

Here is a link to the episode if you want to hear our latest views and macro, a spot Bitcoin ETF, stocks, bonds, and much more. It was a lively discussion, as usual!

——–

Another monthly update for Vailshire clients from me, another discussion about contracting liquidity… (sigh). The news continues to be mostly unfavorable, but I’ll try to also point out the positives.

I’m writing this update on the eve before the latest Federal Open Market Committee (FOMC) release and Jerome Powell’s subsequent news conference… which puts my musings at a disadvantage. In addition, we will find out tomorrow how Treasury Secretary Janet Yellen intends to distribute the massive new round of Treasury issuance. These things should typically be non-events in a capitalistic free market economy, but (sadly) they are of much import in a centrally-planned economy, such as we have in the United States.

Regarding Powell and the FOMC, I expect them to speak of continued sticky high inflation and of their ongoing *heroic* efforts to combat it by being sticky hawkish. That is, they will hold the Federal Funds rate at current levels (5.25-5.50%) and be “data dependent” in case they need to raise rates again… and keep them higher for longer. (Yawn.)

Yellen’s press release will be more interesting and will likely have a material impact on the bond markets. If she borrows most of the Treasury’s desired money by issuing short-dated T-bills, then much of the issuance can be absorbed by the ~$1.1T remaining in the Overnight Reverse Repurchase market. However, if Yellen issues a large chunk of longer-dated Treasuries, then the markets may get jolted by the already massive onslaught of such notes. Buyers may be lacking, which could cause rates on the long end of the Treasury yield curve to rise well above 5% and wreak havoc.

The higher the rates go, the more expensive the ballooning US government debt becomes to service in the short, medium, and long term. Many smart people are concerned that this growing debt spiral can quickly turn into a “death spiral,” which could theoretically cause a rout in both the debt and equities markets.

The good news is that I am less worried about such a catastrophe… at least in the near term.

From my vantage point, the US economy is still resilient–thanks, in part, to massive fiscal spending. Unemployment is low, high yield bond spreads haven’t blown out, oil isn’t crashing, consumers are still making purchases, and employed people still have money to invest. Furthermore, many investors are relieved to finally have a meaningful “risk free rate” as most Treasury yields have exceeded 5%.

If a stock and bond market calamity is to occur, it probably won’t happen until the above-mentioned metrics are trending negatively… and in rapid fashion.

Strategies for how we are positioned to endure and profit from current market conditions are outlined in the next section.

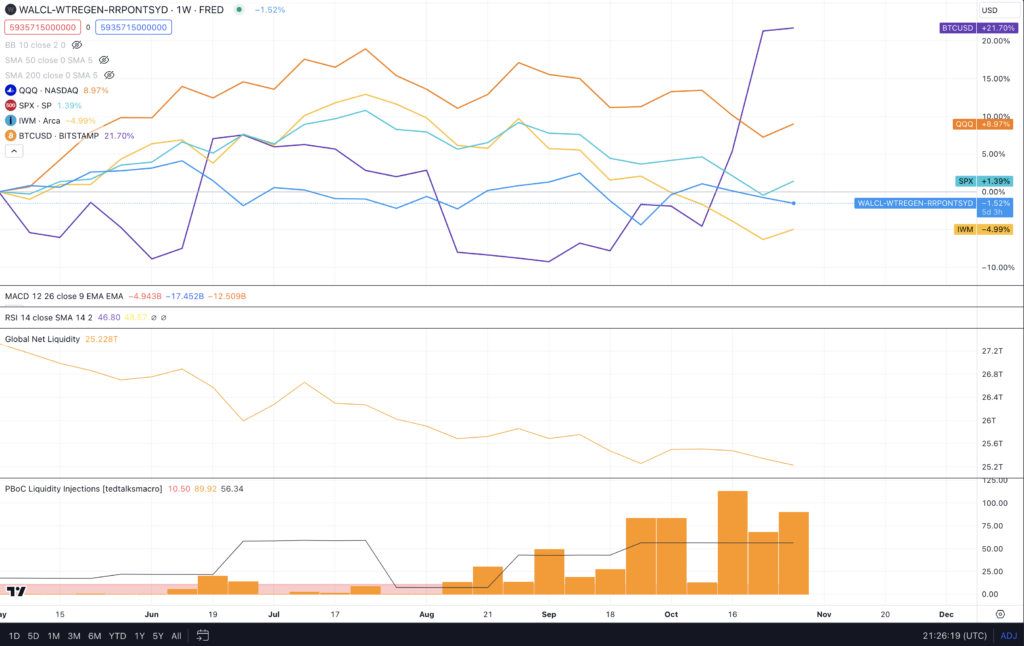

The graph below depicts weekly US net liquidity (blue line), major world bank approximate M2 money supply (gold line in the middle, “Global Net Liquidity”), and Chinese liquidity injections (orange bars, “PBoC Liquidity Injections”) since the beginning of May 2023, compared with Bitcoin (BTCUSD), NASDAQ stocks (QQQ), the S&P 500 (SPX), and US small cap stocks (IWM). — Note that US net liquidity has contracted by -1.5% and approximate global M2 has declined by -7.1%, while China has begun injecting liquidity into its markets. — The best performers include bitcoin (21.4%) and QQQ (9.2%), while IWM (-6.0%) has relatively underperformed.

Strategies for Vailshire’s SMAs

I continue to believe that the 2020s will generally be an unkind decade for stocks and bonds… the bread and butter of typical 60/40 Wall Street portfolios.

Technology and growth stocks have been the only game in town for many years, but they have reached such exorbitant valuations that their future performance is highly suspect; to me, at least.

Bonds were also slated (by me) to perform quite poorly this decade, after a decade-long stint of near-zero or zero interest rate policies (ZIRP). As you may have noticed, Treasuries quickly obliged to this expectation, crashing in price over the past couple of years while their respective yields jumped from 0-1% to 5% or so, where they are now.

In light of these concerns and events, I have used the last month to significantly decrease our overall equity exposure–especially our beloved technology and growth stocks. In addition, and this may surprise some, I have added a new 30% allocation to high yield fixed income ETFs.

I am joyfully adding fixed income because, while I think yields could drift a bit higher from current levels in the coming months, I believe that most of the carnage is over in the bond markets. Since we are not in our new fixed income positions for capital gains but, rather, for meaningful monthly cash income–we will be happy to collect monthly dividends while most of the investment world continues to shy away from such investments.

At current prices, our current ETF combination of taxable municipal bonds (BBN), senior loans (BKLN), and US high yield bonds (USHY), have a combined yield of approximately 7.75%. And if prices dip lower in the coming months, we should be able to add more to these positions… lowering our cost basis and increasing our monthly cash payments via increased relative yields. Exciting stuff!

In case you haven’t heard, Bitcoin is back to fully bullish momentum, which is a good thing. Accordingly, we are once again fully positioned in our bitcoin proxies for now. After the halving in April 2024, I anticipate that bitcoin will start performing exceedingly well for 12-18 months, and we may further increase the size of our positions prior to the bull run. But this remains to be seen and we will tackle it when we get past the halving.

For the above-mentioned reasons, our Vailshire portfolios are now allocated towards a 35% equity, 35% sound money, and 30% fixed income structure. I believe that this three-pronged approach will serve us well throughout this decade of anticipated economic stagnation, high and/or volatile inflation, and eventual credit and monetary expansion.

Here is a summary of our current 35/35/30 “stagflation-busting, income-generating” Vailshire portfolio allocations:

Vailshire’s Aggressive separately managed accounts (SMAs) are allocated as follows (current starter % position size):

EQUITIES (35%)

- 1.5% AAPL

- 1.5% ADBE

- 1.5% AMZN

- 2% AZO

- 3% CALF

- 3% COWZ

- 1.5% GOOGL

- 2% LMT

- 1.5% MA

- 2% MELI

- 1.5% MSCI

- 1.5% MSFT

- 1.5% NVDA

- 2% NVR

- 1.5% SHOP

- 2% TPL

- 1.5% TSLA

- 2% TT

- 2% V

SOUND MONEY (35%)

- 7.5% FNV (gold royalty)

- 15% MSTR (bitcoin proxy)

- 5% WGMI (bitcoin miner ETF)

- 7.5% cash

FIXED INCOME (30%)

- 10% BBN

- 10% BKLN

- 10% USHY

Vailshire’s Moderate separately managed accounts (SMAs) are allocated as follows (current starter % position size):

EQUITIES (35%)

- 1.5% AAPL

- 1.5% ADBE

- 1.5% AMZN

- 2% AZO

- 3% CALF

- 3% COWZ

- 1.5% GOOGL

- 2% LMT

- 1.5% MA

- 2% MELI

- 1.5% MSCI

- 1.5% MSFT

- 1.5% NVDA

- 2% NVR

- 1.5% SHOP

- 2% TPL

- 1.5% TSLA

- 2% TT

- 2% V

SOUND MONEY (35%)

- 12.5% FNV (gold royalty)

- 12.5% MSTR (bitcoin proxy)

- 2.5% WGMI (bitcoin miner ETF)

- 7.5% cash

FIXED INCOME (30%)

- 10% BBN

- 10% BKLN

- 10% USHY

Vailshire’s Conservative separately managed accounts (SMAs) are long-only and are allocated as follows (current starter % position size):

EQUITIES (35%)

- 1.5% AAPL

- 1.5% ADBE

- 1.5% AMZN

- 2% AZO

- 3% CALF

- 3% COWZ

- 1.5% GOOGL

- 2% LMT

- 1.5% MA

- 2% MELI

- 1.5% MSCI

- 1.5% MSFT

- 1.5% NVDA

- 2% NVR

- 1.5% SHOP

- 2% TPL

- 1.5% TSLA

- 2% TT

- 2% V

SOUND MONEY (35%)

- 15% FNV (gold royalty)

- 7.5% MSTR (bitcoin proxy)

- 12.5% cash

FIXED INCOME (30%)

- 10% BBN

- 10% BKLN

- 10% USHY

Vailshire’s Ultra Conservative separately managed accounts (SMAs) are long-only and are allocated as follows (current starter % position size):

EQUITIES (35%)

- 1.5% AAPL

- 1.5% ADBE

- 1.5% AMZN

- 2% AZO

- 3% CALF

- 3% COWZ

- 1.5% GOOGL

- 2% LMT

- 1.5% MA

- 2% MELI

- 1.5% MSCI

- 1.5% MSFT

- 1.5% NVDA

- 2% NVR

- 1.5% SHOP

- 2% TPL

- 1.5% TSLA

- 2% TT

- 2% V

SOUND MONEY (35%)

- 17.5% FNV (gold royalty)

- 5% MSTR (bitcoin proxy)

- 12.5% cash

FIXED INCOME (30%)

- 10% BBN

- 10% BKLN

- 10% USHY

Vailshire’s Bitcoin Proxy separately managed accounts (SMAs) are allocated as follows (current starter % position size):

- 95% MSTR (bitcoin proxy)

- 5% cash

**As written in prior emails and client updates, SMA clients in FL and TX remain in cash-only positions as Vailshire awaits state-specific regulatory approval to begin/resume investing on behalf of these client accounts. Our legal team is doing everything in its power to get this approval as quickly as possible. I am sorry for the ongoing delay in trading/investing for Vailshire’s FL and TX clients!

If you are a Vailshire client, feel free to log in to your account(s) at Interactive Brokers and see how your own portfolios are positioned. (It’s a good idea to log in and review your account(s) at least quarterly, just to make sure your settings and demographics are up to date.)

Conclusion

Another Fun Mastermind Discussion!

Liquidity continues to dry up and bond rates have soared. These, among many other factors, suggest that this is not a time to be overly aggressive with our investments… or overly bearish, for that matter. It is a crab market after all.

We have made some material changes to our Vailshire portfolios to deal with and hopefully thrive within the tumultuous current and coming economic and geopolitical conditions. I hope that you are able to rest easy and even share in my optimism for the days to come.

As always, I am incredibly thankful for you and the confidence you have placed in Vailshire to manage your hard-earned capital. I will continue doing my best and working hard on your behalf.

Living well and investing wisely with you,

Jeff Ross, MD/MBA